FACETS Data Sources – March 2023

Data has been drawn from high quality, publicly available sources, as detailed below. The dataset describing existing electricity generating units is drawn from the EPA National Electric Energy Data System database (NEEDS). Hydropower plants, existing wind and solar, and small gas and oil units have been aggregated by model region. All other plant types are represented at the unit level. The model may economically retire existing units whenever they are not part of the least cost solution relative to other options for meeting demands.

Each existing plant is tagged with its latitude and longitude, so that unit-level results can visualized. Existing units have been geo-located in the 134 balancing areas (BAs) of the National Renewable Energy Laboratory (NREL) ReEDS model that form the basic regional structure of FACETS. Both existing inter-regional transmission capacity and investment options for capacity expansion are specified, enabling analysis of the costs and benefits of connecting renewable resources with distant loads.

The model can build new plants from a suite of options whenever it finds it cost effective to do so. New plant options (with the exception of new wind and solar) are drawn from Annual Energy Outlook (AEO) input data. PV, wind, and battery storage cost and performance are taken from the NREL Annual Technology Baseline 2021 scenarios. Supply curves for wind and PV installations are drawn from detailed ReEDS model data at the level of the BAs for PV and sub-regions of BAs for wind. Each region's supply is broken up by class and cost of grid interconnection, making a rich supply curve of nearly 3000 options for PV and over 10000 for wind. Each supply step's production is characterized by an 8760 hourly generation profile, which is then aggregated into model time slices. Inflation Reduction Act tax credits for new facilities, existing nuclear units, and carbon capture and storage have been reflected in model costs.

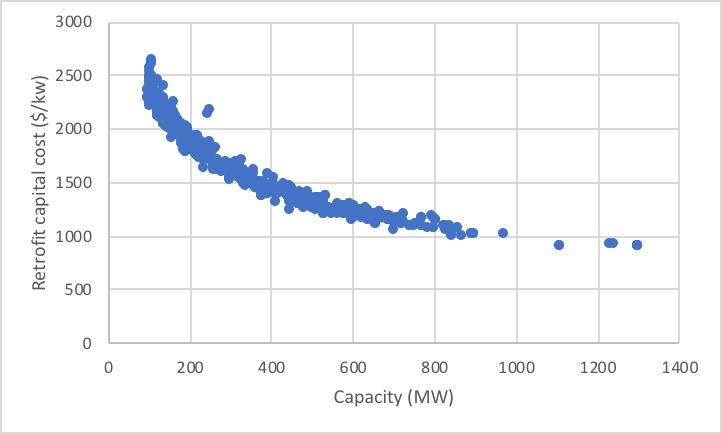

Carbon capture and sequestration (CCS) retrofits are available for individual existing coal units with capacity 100 MW or greater. The cost methodology was developed by Clean Air Task Force (CATF), based upon the Petra Nova retrofit experience. An auxiliary gas unit provides steam for the CCS system, avoiding a heat rate penalty to the coal unit. Emissions from the gas unit are not captured, reducing the effective capture rate from 90 to around 79 percent. Retrofit capital and operating costs and gas and electricity needs for the CCS system are all scaled to the required daily carbon capture rate. The graph to the right shows the range of retrofit capital costs versus capacity for eligible units.

Captured carbon for new or retrofitted plants may be utilized for enhanced oil recovery (EOR) or stored in saline aquifers. EOR supply curves were developed by ARI and CATF. Four steps of EOR are available at $45, $30, $15, and $0/ton payments for CO2 delivered to 9 oil basins. EOR supplies are tied to oil prices, such that in the AEO 2017 Reference oil price case, all EOR potential is available immediately, whereas in the Low oil price case, EOR potential ramps up gradually over time. Estimated industrial CO2 supplies have been netted out of the EOR supply curves. Pipeline transport costs on a $/ton basis from power plants to EOR basins were developed by CATF, based upon distance, terrain, and assumed diameter for each route. Regional supply curves for saline storage of captured CO2 and transport costs between power plants and storage sites are derived from EPA’s IPM model 5.13 Base Case.

Coal supply, quality, and transportation cost information have been drawn from EPA IPM v6 Base Case and its updates. There are 70 different coal types, distinguished by grade, sulfur content, and 37 supply regions. Non-power sector coal demands, as projected by AEO and IPM, including exports, are deducted by the model from these supplies. Coal plants are assigned applicable coal grades (bituminous, subbituminous, and/or lignite) based upon NEEDS data. Unit-level SO2 permit rates and any SO2 removal equipment, also drawn from NEEDS, restrict the sulfur content of fuels available to each plant.

Stepped supply-cost curves for natural gas are built from quantities and elasticities derived from AEO scenarios. Alternate trajectories for shale and tight gas are calibrated to the AEO Reference, High Resource, and Low Resource cases. Regional gas delivery markups are drawn from EPA IPM v6.

Electricity loads and load shapes are specified at the BA region level, based upon 2010 county-level load data from NREL. These loads are used to compute the share of each state's demand taking place within each of its constituent BA regions. These shares are then held fixed in time, and state-level demands are projected using AEO electricity consumption growth rates by Census Division. A distribution loss of 5.3% is charged on all electricity delivered from the transmission grid to state-level demands. An alternate model formulation derives electricity demand endogenously from device choices in the end-use sectors.

Endogenous energy efficiency opportunities are specified as state-level supply curves for $/MWh saved. Potentials are derived from EPRI’s State Level Electric Energy Efficiency Potential Estimates study. EPRI provided economic potential without and with additional incentives. For FACETS, we broke the economic potential available with no further incentive into three equal cost steps, assigning costs derived from the LBNL 2015 Total Cost of Saved Energy study to the three steps. We then added two further steps consisting of the additional potential EPRI estimated to be economic at incentives of $10 and $20/MWh. EPRI estimated that approximately 20% of their potential was "naturally occurring" within AEO projections. This portion of the potential was netted out equally from the first three steps. The resulting potential as a fraction of total national load grows from 7.3% in 2020 to 18.3% in 2050.

Cost and performance characteristics for light duty vehicles (LDVs) in 12 size classes and a variety technology types are drawn from AEO. Scenario analysis considers cases in which electric vehicle (EV) costs reach upfront cost parity with internal combustion engine vehicles at various points during the model horizon.

Existing LDV fleets are built up at the state level based on AEO total stocks and US EPA National Emissions Inventory (NEI) data, along with US DOE data on hybrid and EV registrations. These base year fleets are apportioned to AEO size classes using AEO and state registration data and to a vehicle age distribution based on NHTSA vehicle survivability data. FACETS then tracks fleet turnover and purchases new vehicles as needed. Size class shares from the AEO Reference and High and Low Oil Price cases are imposed on sales.

Five levels of EV charging infrastructure investment requirements are imposed at the state level to allow for increasing penetrations of EVs. Three are drawn from NREL’s 2017 National Plug-In Electric Vehicle Infrastructure Analysis and two are based on the percentage of state households living in multi-unit dwellings (MUDs) and assumptions about the number and type of MUD chargers required per MUD EV.

State EV fleets are assigned to counties based upon their shares of state urban and rural population. According to data from NRELs Infrastructure Analysis, in 2016, 91 percent of existing EV registrations are in urban areas, with only 9 percent in small town and rural areas. These percentages are used to assign model EV purchases to counties in the early years of the model horizon. Over time, the shares evolve to the current ratio of all vehicle registrations: 71 percent urban and 29 percent small towns and rural. These county fleets are then used to link EV charging to the model’s electricity supply regions.

LDV charging profiles available in FAcets

Three LDV charging profiles are available for testing, based on profiles developed by NREL for their RE Futures study. In the At Home profile, all drivers plug in when they reach home, resulting in charging loads that peak in the early evening, exacerbating system peaks. The Opportunity profile assumes that widespread EV charging infrastructure allows drivers to plug in throughout the day, whenever they have an opportunity, resulting in a flatter daytime load. The Late Night profile assumes that utility time-of-use pricing induces drivers to postpone charging to the late night hours. The model can also optimize charging based on dynamic electricity pricing.

Heavy duty vehicle (HDV) fuel consumption and emissions are projected based on AEO 2018 vehicle miles traveled, vehicle efficiencies, and fuel shares for light, medium, and heavy duty commercial trucks and school, transit, and intercity buses. Electric vehicle options and associated infrastructure investment costs for each vehicle category are based on NREL’s Electrification Futures Study moderate technology case. Using an approach similar to NREL’s, three scenarios for electric HDV penetration were developed, based VIUS 2002 typical daily range data for trucks and travel type for buses. Electric HDV charging loads are assigned to model electricity supply regions based on county shares of vehicle miles traveled in the EPA 2014 NEI data.